Newsletter for Web3 Investment in Africa

Africa’s SME Lending Boom and Web3 Approach

Dear reader,

Welcome to the inaugural edition of the EMURGO Africa Web3 Newsletter where we kickstart the journey of bringing you the latest analysis about the continent's Web3 landscape. We aim to lead on this prong in a captivating and inclusive manner. Our first edition takes you through Africa’s Web3 lending landscape.

Key Takeaways

- Demand for short-term loans from blockchain-based projects is set to grow faster in the next 6-12 months thanks to their competitive rates.

- Competition intensifies between Web3 lending startups and non-blockchain fintechs led by Safaricom’s Faraja and PayFlex.

- Safaricom, Flutterwave and MTN are expected to expand SME lending services in the next 12 months.

- Lending on blockchain helps lower interest rates, creates a new way of collateralization and attracts more SME borrowers.

- Web3 approaches to collateralization and risk management are also making emerging-market lending more attractive to a wide range of investors.

Tougher Economic Indicators

Africa’s micro, small and medium enterprises (MSMEs) face enormous challenges to sustain their daily operations due to recent economic backdrops. The continent’s major economies see rising inflation, weakening local currencies to the US dollars, high foreign debts, and slowing GDP growth.

Nigeria, Africa’s largest economy, saw a 2.4% year-on-year GDP growth in Q1 2023, slower than its 2022 annual growth of 3.3%. South Africa recorded a growth of 0.4% in the January-to-March quarter. The World Bank has trimmed Egypt's real GDP growth rate to 4% this year from 4.5%, while the nation saw a 6.6% rise last year. Kenya’s economic growth fell in the same quarter to 5.3% compared with 6.2% a year earlier.

Many MSMEs in these economies struggle to scale their businesses due in part to cash constraints. The lack of sufficient operating capital means they can’t grow their market size fast enough to attract potential angel investors or venture capitalists.

The cost of credit in Africa has gone up as central banks attempt to ease inflation and reduce pressure on local currencies. As loans from banks and microfinance institutions become costlier, some of the SMEs have found refuge in Web3 lending platforms, which offer credit at lower rates. Blockchain lending also eliminates the need for a credit score to acquire a loan.

Table1.1

Inflation and bank rates

SOURCES: World Bank, Fitch, Trading Economics, Central Banks of Nigeria, Kenya, Egypt, South Africa, Ghana

NOTE: Central Bank lending rate is either lower or higher than the rate commercial banks offer. In Kenya, for instance, commercial banks’ rate is capped at 4% higher than the central bank rate, which moves it to 14.5%. In South Africa, commercial banks can offer interests of between 3% and 23.9% despite the central bank maintaining a rate of 8.2%

Inflating Credit Costs

The liquidity problems persist in Africa as most SMEs get their initial capital from bootstrapping and support from family and friends. This is because they can't access credit from traditional sources. Data by the African Development Bank shows that 44% of all credit obtained by people in sub-Saharan Africa is from their relatives.

Interest on traditional bank loans for SMES across Africa range from 10% to 49% per year, with an average pegged around 15%, according to our research. Accessing financing from banks and microfinance institutions is relatively expensive, time consuming and a default trap. Moreover, the majority of SMEs struggle to prove their creditworthiness to traditional lenders.

Traditional Microfinance institutions (MFIs) play a bigger role in financing MSMEs in Africa but charge higher interest rates and give borrowers a shorter payback period. Some MFIs in Kenya charge as high as 10% per week, refundable in one month. This translates to 520% per year.

Most commercial banks in Africa have raised their lending rates in the past 12 months to tame inflation. According to our research, interest rates in Nigeria were hiked from 14% to 18.75% in July 2023. Kenyan banks also raised their rates from 12% to 15% in July. Ghana’s lending rates hit an all-time high of 29.5% in August, while Madagascar holds the record of the highest bank interest rate in the continent at 48.8%.

The total loan cost comprises not just the cost of the original loan and the interest charged but also the transaction costs, like fees for lawyers to perfect collateral.

Table 1.2

SME Lending Rates by Africa’s Biggest Commercial Banks

Sources: Standard Bank, Access Bank, GCB Bank, Equity Bank, Banque Misr

As a result, an estimated 28.3% of SMEs in Africa are fully credit constrained. They can no longer qualify for more loans from banks, microfinance institutions and fintechs due to a history of credit defaults. Such situations have forced many SME owners to close shop, leading to a loss of livelihoods in a continent where unemployment rates are the highest in the world.

Standard Bank, Africa's biggest lender by assets, reported that its loan losses for the first half ended June 30 jumped by more than 40%. Data from Kenya’s Business Registration Service (BRS) show that over 2,000 SMEs closed down in the past 12 months alone. In the past five years, 9,400 businesses have been deregistered in Kenya mainly because they could not access finances to run their normal operations.

The same reason led to the closure of over 600,000 MSMEs in Nigeria in 2022. Yet, most SMEs in Nigeria are not registered at all, meaning they are not credit eligible due to lack of data. There were 1091 liquidations in South Africa last year despite the country’s upper middle income economic status.

The Emergence of Web3 Lending

Table 1.3

Sources: Central Bank of Kenya, Central Bank of Nigeria, CEIC Data

However, several startups using blockchain technologies are offering SMEs loans at more friendly terms, interests, and transaction fees. Blockchain-based lending opens a new approach to collateral and credit scoring, making more SMEs eligible. In Web3 lending, there are no intermediaries to make the loan application process expensive, and the global interest rates are between 2% and 6% per year, compared to banks, which offer double digit rates.

Globally, according to McKinsey & Co, more than $200 billion in loans was disbursed in 2021 from the largest Web3 lending platforms—and cumulative bad debt is currently roughly $1 million, despite significant volatility. This puts the default rate at an insignificant 0.000005%. The global Web3 space was valued at $934 billion in 2022, while the global retail banking market size was estimated at $1.9 trillion last year.

Web3 Lending Mechanism

Why is Web3 lending becoming popular? One reason is there are no upfront costs such as loan application fees or legal processing fees in applying for the loan provided by Web3 projects. But the major reason lies within the fact that all terms of the credit facility, including interest paid and liquidation thresholds, are predetermined by a smart contract which is available transparently to all participants.

A smart contract is a piece of computer code stored on blockchain that runs when predetermined conditions are met. It is used to automate the execution of a transaction between parties without any intermediary’s involvement or time loss.

With Web3, token owners stake their funds to earn rebates on their deposits for a particular period of time. They hold their funds in a non-custodial wallet that represents an account on the blockchain network. Web3 lending allows people to borrow funds from a pool of lenders. The lenders receive yield from the interest borrowers pay.

Interest rates paid by borrowers, therefore, no longer accrue to management and shareholders. This interest is governed by a blockchain startup that often has no claim on any of the revenues. The interest on loans is paid into the smart contract and disbursed back to the original depositors of the liquidity.

The smart contract itself accrues zero revenue, but sometimes will accrue a small spread used for insuring funds. The price of the underlying collateral for the loan has been falling in recent years, with loan liquidations being triggered automatically by each smart contract without creating delinquencies associated with each loan. This substantially reduces the interest rate on every loan.

Africa’s Tech Giants Vs. Web3

Fintechs in the continent cannot afford to miss out on the expanding SME lending market. Africa’s two largest telecom giants, Safaricom of Kenya and South Africa-based MTN Group are among the non-blockchain SME lenders.

Safaricom, Nigeria’s Flutterwave, MTN’s MoMo in Ghana, South Africa’s Jumo and PayFlex, and Botswana’s Leshego have all operated loan products targeting SMEs. To emphasize the significant roles this fintechs play in the lending business, Mastercard bought a minority stake in MoMo in August. This saw the valuation of MoMo rise to $5.2 billion, making it the most valuable fintech company in Africa.

And while these fintech firms have managed to offer most SMEs access to funds that seem affordable on paper, the terms and conditions for the loan facilities may not be favorable.

Many credit products by these fintechs offer a lower interest rate of as low as 5%, but that is per month. This makes them even more expensive than commercial banks that offer double digit rates per annum. Failure for SMEs to refund the cash within 30 days, for instance, in the case of Flutterwave, attracts further charges, and on average it could blow up to 60% per annum. That means if an SME was loaned $1,000, it will refund $1,800 which further negatively impacts on its liquidity and profitability.

Table 1.4

Lending Rates by Big Techs and Fintechs

Sources: Homepages of the lending services by the above companies

Even Kenya’s Safaricom, East Africa’s biggest company by market capitalization, which launched a loan facility dubbed Faraja for SMEs in July isn’t as cheap as it appears.

The company offers free business loans for 30 days via its popular M-Pesa mobile money platform on a Buy Now Pay Later mode, capping the amounts at $700 per business but those that fail to pay up within the moratorium period are struck with a suspension from the platform. The company then engages a debt-collection agency to recover the amount in default.

While Botswana’s Letshego allows SMEs up to 3 years to repay their loans, at 17.5%, its interest rate is just as high as that of commercial banks, only that the application process is less bureaucratic.

Web3 Deals Tracker: Pezesha Raises $12.8 Million

Now, the continent is warming up to Web3 lending solutions, which provide better interest rates, favorable modes of repayment, and lower transaction costs. At a time when such funds are hard to come by, venture capitalists have been flocking into the continent in the past two years, to finance startups that offer peer-to-peer lending to SMEs.

Through this frontier means of lending, traditional financing protocols get bypassed, affording SMEs the cash to operate and expand. This in turn creates more employment opportunities in the process. It should be noted that up to 90% of the population in Africa is employed by SMEs. The use of stablecoins in the Web3 lending process, though still in its nascent stage, is proving to be a sure way of cushioning SMEs against the existential threats of shutting down.

Table 1.5

Notable Web3 Lending Projects and VC Funding

Sources: Pezesha, Paylend, Jia, P2Vest, Sycamore, Oze__ *Pezesha partners with Kotani Pay for Web3 lending service.__

At $12.8 million, Pezesha has raised the highest capital for this kind of business so far. Kotani Pay, which works alongside Pezesha, closed a $2

million pre-seed funding round led by P1 Ventures in early September.

In the next 12 months, the demand for lending facilities among SMEs in Africa is expected to rise. And this comes with more competition between fintechs and Web3 lending companies, as they seek to onboard more users.

In Kenya, for instance, Safaricom’s loan product for SMEs, Faraja, started in July. This came months after the government launched its own version of affordable loans for SMEs dubbed Hustler Fund.

The Hustler Fund government project allows groups to apply for loans ranging from $140 to $7,000. The interest rate is 7% per annum on reducing balance and an additional 1.5% for those who fail to pay in time. The repayment period is six months from the disbursement date.

Now, with Web3’s demonstrated lower rates in the country, more SMEs are expected to start seeking credit from them.

“This is catching up, because those who lend to SMEs on Web3 platforms are already getting rewards for it. I see an inflow from traditional banking to Web3 in the next 12 months, but there’s a long way to go because education is needed to create mass awareness among SME owners,” Eliutherius Juma, CEO of Paylend says.

In South Africa, where 40% of the population is familiar with the concept of Web3, according to a 2023 survey by ConseySys, decentralized form of lending is expected to grow in the next 12 months. The report states: “80% of the population of South Africa agrees that we currently have the technology required to transform or fully rebuild the financial system.”

South Africa is also Africa’s most Web3 friendly country, having passed regulations to govern the industry. This is expected to draw more investors in Web3, especially in the field of financial services.

Since electing a new government, Nigeria has been embracing blockchain technology and decentralized finance (DeFi). As the Central Bank of Nigeria continues to recognize the potential benefits of DeFi lending and real-world asset tokenization, such as increased access to finance and economic growth, it is expected to adopt a more supportive stance and develop regulations that promote Web3 innovation and consumer protection.

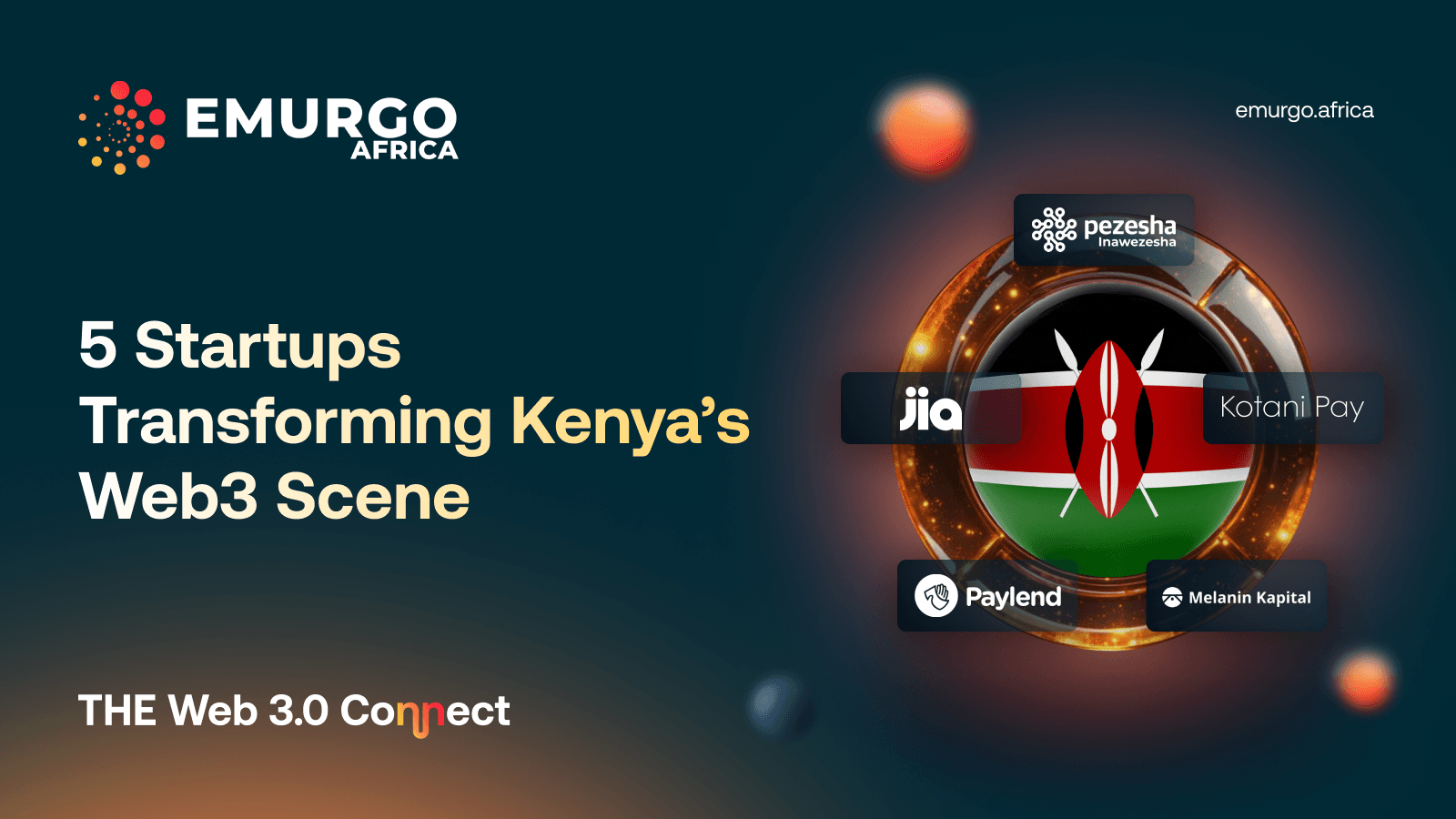

How Africa’s Web3 Lending Platforms Work

- PEZESHA

Pezesha is a Kenyan Web3 lending digital marketplace that connects SMEs with investors or lenders offering affordable working capital. It runs on the Celo blockchain platform and offers loans in the Celo stablecoin (Celo dollar or cUSD). To access it, users need to download the app from Google Play Store and register. They will then go through a credit score check to determine business loan limits. The user requests for a loan, which Pezesha automatically asks lenders to provide. The user gets a matching investor and who offers the loan in minutes. The money reflects in the user’s online wallet. But the user’s business must have been operating for at least 6 months to qualify for a business loan.

Since going live in 2017, Pezesha has connected more than 20,000 youth MSMEs with working capital, leading to the creation of more than 1,000 formal sector jobs and 5,000 informal sector jobs. Pezesha has funded more than 75,000 loans to MSMEs, and educated more than 200,000 MSMEs across Kenya.

Since 2021, it has worked with Kotani Pay, another startup that makes it easier to integrate through its secure APIs that support SME lending protocols. It is integrated with the Celo, Stellar, and Avalanche blockchain networks. Using USSD for feature phones, the startup brings financial instruments and services to small businesses that do not have access to the internet or have the capital and credit standing to open a bank account, thus increasing financial freedom.

2. PAYLEND

Paylend runs a loan product called Inua Biz which enables business owners to access low-interest loans to grow their business, and achieve business liquidity. Users are required to sign-up on the web or via mobile app and start accessing credit on a peer-to-peer platform. It also allows users to buy goods on credit from local retail shops using crypto. Both the buyers in the community and retailers are hosted on the same platform. Consumers can see which shops offer credit facilities from the platform. Paylend has served 5,000 SMEs so far in Kenya. It plans to expand to Nigeria, Tanzania, South Africa and Zambia.

3. JIA

Jia is trying to replicate the model of community finance (table-banking) groups, which are popular in markets like Kenya, where members, who are borrowers too, hold shares and earn from the groups. Jia turns crypto liquidity into working capital for small businesses in emerging markets. Each crypto token, called Jia point, has a claim to a stream of revenues from Jia’s lending protocol. Jia points are claimable once the token-system is fully established. Meanwhile, borrowers can use them as security for lower interest rates, higher loan amounts and more flexible loan terms. Jia employs an automated underwriting model to evaluate potential borrowers, and deploys financing to them from on-chain liquidity pools backed by global investors. Investors supply capital and earn sustainable yields backed by real-world businesses and assets. Borrowers apply to receive financing and resources to support business operations.

SMEs and Mobile Money Are Africa’s Backbone, Stats Show

l According to the International Finance Corporation (IFC), MSMEs account for over 90% of businesses and more than 50% of employment worldwide. Despite their huge contribution to economic growth, MSMEs face a financing gap of over $8 trillion globally.

l In Africa, SMEs provide an estimated 80% of jobs across the continent, representing an important driver of economic growth. Sub-Saharan Africa alone has 44 million MSMEs. SMEs account for 98.5% of all businesses in South Africa. In Kenya, they make up 98% of all businesses in the country, while in Nigeria MSMEs comprise 96.7%.

l Approximately $832 billion was transacted through mobile money in Africa in 2022, accounting for about 65.8% of global mobile money transaction value of $1.26 trillion in 2022, according to the GSMA. Digital transactions are on the rise as the use of cash slows down. Total transaction value for mobile money grew by 22% between 2021 and 2022. The African mobile money growth rate is the same as the global average of 22%.

l Startups in Africa employing blockchain-related technologies raised a total of $474 million in 2022, compared to $89.6 million in 2021. This translates to a fivefold rise.

QUOTES OF THE MONTH

“The idea is to provide affordable financing for micro-businesses, and when they repay, they become owners by getting token rewards.” - Zach Marks, Jia CEO and co-founder.

“In the early days of crypto adoption in Nigeria, we noticed that USDT had great traction especially when we analyzed the volume of transactions for small businesses adopting USDT. We understand how we can implement the different stablecoin-based solutions on Cardano Network and we are focusing on the innovation powered by stablecoins and the interoperability across multiple platforms to create ease” - Oyedeji Oluwoye, co-founder of Canza Finance, which is among the Web3 startups in Africa that plan to build the continent’s financial system using blockchain technologies.

THE Web3 Connect is produced by EMURGO Africa’s research team: Faustine Ngila, Africa Editor at NODO; William Phelps, Investment Manager of Adaverse; Mayuko Kondo, Tech Scientist at EMURGO Africa; Omar Badr, Marketing Director of EMURGO Africa; Shigeru Sato; Chief Content Officer at NODO.

DISCLAIMER: The information in this content (website or other form) does not represent an offer or commitment to provide any product or service. The analysis, opinions and estimates expressed in this content are those of the respective authors, and may differ from those of EMURGO Africa and/or other EMURGO Africa employees and affiliates. Copying, re-publishing or using this material or any of its contents for any other purpose is strictly prohibited without prior written consent from EMURGO Africa.